In late February, war broke out in the Middle East, quickly escalating to a global energy crisis by Iranian blockade at the Strait of Hormuz. As a key maritime passage, its gatekeeper has vast power in global trade, utilised to Iran’s full extent after their supreme leader Ayatollah Ali Khamenei was killed in bombing by US forces on February 28th to disrupt Iranian leadership [1]. Iran has since performed counterstrikes across the gulf region, targeting various military and civilian goals. Targets on desalination and nuclear facilities are causing major cause for concern, their damage enough to disrupt drinking water supply for millions, or worse, spread nuclear waste and radioactivity throughout the region and beyond [2]. Not only would it hinder electricity generation, it could cause major public health issues for decades if not handled properly [3]. This article argues that the Strait of Hormuz crisis represents a classic negative supply shock with global consequences, reshaping inflation, trade flows, and geopolitical power balances.

Strategy Behind the Strait of Hormuz

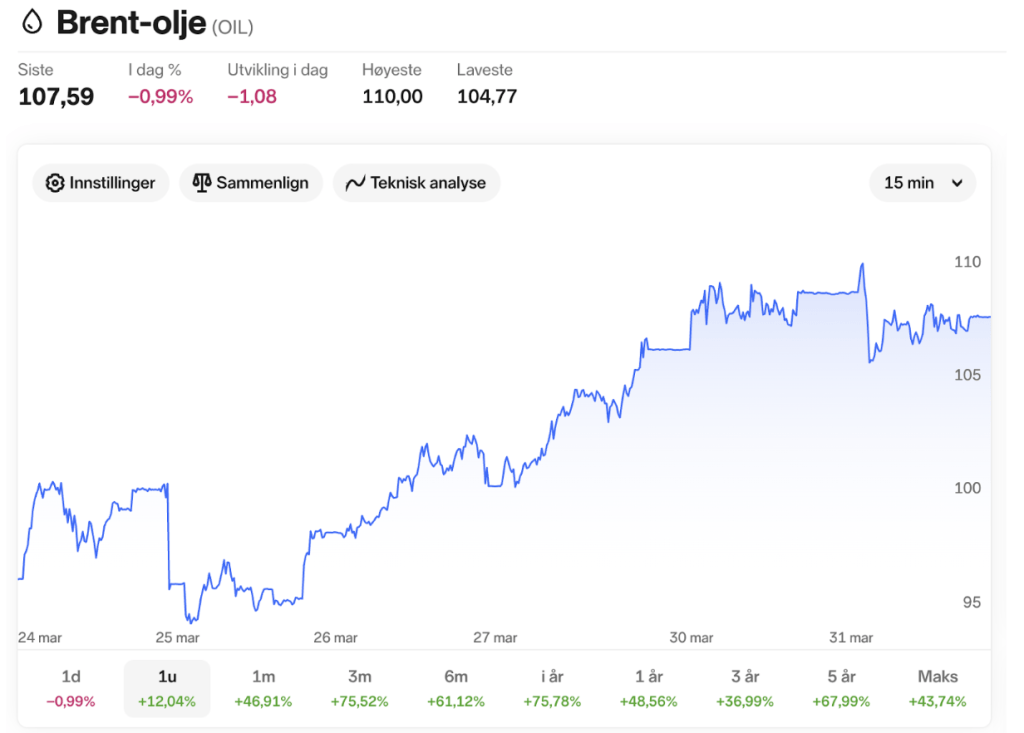

While the war is mostly confined to the Middle East, it has ripple effects on the world economy, as seen by palpable volatility in oil prices. This volatility reflects the barricading of the Strait of Hormuz by Iran and is limiting many countries’ access to oil. Brent crude oil is a vital commodity worldwide and its barrel price functions as a metric for global oil pricing. Currently trading at a staggering USD 107.59 per barrel (April 1st), it is up from USD 73.24 on February 27th. That’s as much as a 47% price increase, reflecting investors’ assessment on the impact the war in the Middle East has on global supply [4]. To understand why this disruption is so significant, it is necessary to examine the strategic role of the Strait of Hormuz.

The Strait of Hormuz is the corridor connecting the Gulf with the Arabian Sea, only as wide as 33km at its most narrow point. While Iran lies on the upper side of the strait, Oman controls the lower tip. Dubai, on the Emirates’ coast is situated at the very entrance of the strait. Currently blocked by Iran, the strait is …”one of the world’s busiest oil shipping channels” [5]. As much as 20% of the world’s oil and liquified gas passes through the strait, meaning the blockade affects a vast amount of the energy market, causing prices to skyrocket [5]. This disruption in supply translates directly into what economists describe as a negative supply shock.

(Crude Oil Price on March 31, via Nordnet)

The Economy of Oil Shocks

Rising oil prices transmit inflation across nearly all sectors of the economy. This rapid price increase in crude oil reflects a negative supply shock. Not only does it affect industries, but also consumers – lowering individual buying power. This could in turn reduce aggregate demand, causing an additional downturn of the economy [6]. Central Banks worry that high oil prices could steer the world into another recession, having just weaned off the last since the covid pandemic. As such, oil prices affect price levels not only in the energy market but in the global economy. An example of the potential effects of a heightened barrel price is discussed beneath.

Global Economic Impact

The acclaimed Oxford Economics ran a simulation based on the worst-case scenario of an oil price average of USD 140 per barrel for a 2-month period. Correlation between oil prices and stock market prices would cause the tightening of the financial market. This would lead to inflation and increase in fuel costs, food and other goods, lowering the overall spending in the economy, and causing a secondary wave of decreased economic activity. Supply chain stress would also ripple through Asian and European exports and imports, as well as causing less travel in and through the Middle East – all implying lowered global economic activity. At the oil price level of 140 USD per barrel, only a few months would send the whole world economy into a mild recession. This is however only estimations, and the course of the war will ultimately show whether oil prices will reach this level, or increase beyond it, and the severity relating to the duration of such levels [7].

Winners, Losers, and China

Oil importing countries such as India, Japan and much of Europe may face higher fuel costs, inflationary pressures, and trade deficits as a result of the war, as well as international trade, shipping, logistics, and airline companies. Stock markets will face volatility in the short term and even reduced investment in the long term. On the flip side, however, are the winners of the war.

Oil exporting nations, such as Russia, Canada, and Norway may benefit from higher oil prices, thereby boosting their currencies. Big energy companies such as ExxonMobil and BP might also experience bigger profits, leaving investors more likely to invest in the energy sector. Arms manufacturers globally might see increased profits overall. Gold and the US dollar are also likely to strengthen in times of uncertainty [8].

While China is the world’s largest importer of oil, and would normally bleed from this war, they are willing to trade with Iran and Russia for their oil, despite sanctions from other countries [9]. According to The Economist, Iran earns almost double the amount of profits from oil now than it did prior to the outbreak of the war, largely due to the price increase [10].

Sanctioned countries may sell at a discount, allowing China lower input costs more than the global average – retaining and sharpening the competitive edge they already have. China is uniquely able to position itself as a neutral economic partner which will likely serve its stability in the long term [11]. Overall, the crisis redistributes economic advantages, benefiting only a handful of energy exporters while placing significant strain on import-dependent economies.

Global Policy Responses

The Organisation of the Petroleum Exporting Countries (OPEC) was quick to respond to the outbreak of the war, and OPEC+ decided on March 1st to boost oil output with 206 000 barrels of oil per day from April onwards. Considered a modest boost, OPEC+ increases supply by adding barrels in time of need, but analysts claim the group has “little spare capacity to add to supply.” The agreed amount, just in excess of 200k barrels, will only represent around 0.2% of global supply. According to Reuters, this might not be enough to stabilise the market. Saudi holds OPEC’s spare production capacity and is increasing its production by 500 000 barrels in recent weeks. Due to the blockade of the Gulf however, Saudi needs to utilise its access to the Red Sea. While this is fully possible, Saudi cannot deliver at its full capacity without access to the Gulf. Less fortunate oil-producing Gulf nations do not have access to any port, neither on the Gulf or Red Sea coast [12].

In order to counteract the steep price-increase in oil, nations around the world are releasing their strategic oil reserves. According to IEA, the International Energy Agency, its 32 member states have “…unanimously agreed […] to make 400 million barrels of oil from their emergency reserves available to the market…”. It’s the largest oil stock release ever, done as an emergency decision to reduce disruptions in the oil market. It represents 22% of total global observed oil stocks. The emergency stocks will however take time to be released on the market, left undefined by the IEA [13]. In hopes of calming the global economy, the IEA hopes to influence consumer spending, stabilise currencies, and control inflation worldwide, by reducing the volatility of the commodity and input variable that oil represents in today’s world [14]. Countries such as the US are looking elsewhere to ensure continued access to oil. Having recently removed Maduro, the Trump administration now has close ties to the new Venezuelan government and has secured access to their natural resources. Many American companies are also signing agreements with the Venezuelan government to secure a steady supply of oil [15].

Is The Cure for High Prices Really High Prices?

While OPEC and the IEA try to artificially stabilise the market by external input from strategic oil reserves and increased spare capacity, there is also the economic consensus that a truly free market is self-correcting – stating that the cure to high prices is high prices, as demand naturally lowers when input costs are high. The energy market however is not a free market. It is a cartel with significant market power run by OPEC, the world’s oil producing nations. In this way, OPEC nations have full power to set prices and demand as they wish as long as they can manage surpluses and shortages non-existent in free markets [16]. While this allows them to control and cooperate amongst themselves it requires manual adjustments when the market is halted by war and other disruptors. High prices in this case may not self-correct by other high prices, due to the necessity of the commodity. If the price stays high in the aftermath of the war and shows more permanency, then it will send the world economy into a deeper recession and cause people and corporations around the world to adjust to higher expenditure costs, not a privilege for all.

Conclusion

The strategic significance of the Strait of Hormuz is exactly why Iran is utilising it to pressure Israel and the US, while also causing spillover effects on the rest of the region and the economy at large. Energy importers reliant on Middle Eastern energy, or energy passing through the strait, are reminded of just how vulnerable they are to shifting supply. The Suez and Panama channels, and the Strait of Malacca are other such examples. The current war exemplifies the power of controlling access to them.

Depending on the length of the war in the Middle East and the related high energy prices, countries largely depending on trade partners for continuous energy supply may look inwards and try to solve these issues domestically. As such the world might become more protectionist in an attempt to rely less on trade and trade partners.

The issue that could arise from this protectionism relates to Montesquieu’s classical liberalism, as stated in “The Spirit of the Law” (1748) where peace is a natural effect of trade. It is due to the mutual economic benefits of trade and dependence that comes from relying on each other [17]. While a trade imbalance might provide leverage and power to some nations, both sides have an incentive to avoid conflict. In order for the world to remain at peace it is therefore vital that international trade occurs. When sovereignty is breached however, like by the bombing of another nation’s supreme leader, the rules of the game have already been broken, sovereignty breached, and thus, retaliation expected.

Edited by Adrian Kai Fraile Itagaki.

References

MODIS Land Rapid Response Team, NASA GSFC, Strait of Hormuz and Musandam Peninsula.https://commons.wikimedia.org/wiki/File:Strait_of_Hormuz_and_Musandam_Peninsula_(MODIS_2018-12-10).jpg. Accessed 21 Mar. 2026.

“Nordnet Oil Indicator.” Nordnet, https://www.nordnet.no/market/indicator/oil. Accessed 31 Mar. 2026.

[1] Ewing, Giselle Ruhiyyih. “Ayatollah Khamenei Is Dead. Here’s What That Means for Iran’s Leadership.” POLITICO, Politico, Mar. 2026, http://www.politico.com/news/2026/02/28/ayatollah-khamenei-iran-leadership-00806167. Accessed 21 Mar. 2026.

[2] Hussein, Mohamed A. “How Much of the Gulf’s Water Comes from Desalination Plants?” Al Jazeera, 12 Mar. 2026,https://www.aljazeera.com/news/2026/3/12/how-much-of-the-gulfs-water-comes-from-desalination-plants. Accessed 31 Mar. 2026.

[3] Parliamentary Office of Science and Technology. Assessing the Risk of Terrorist Attacks on Nuclear Facilities. Report 222, July 2004, https://www.parliament.uk/globalassets/documents/post/postpr222.pdf. Accessed 31 Mar. 2026.

[4] “Nordnet Oil Indicator.” Nordnet, https://www.nordnet.no/market/indicator/oil. Accessed 31 Mar. 2026.

[5] Butler, Gavin. “What Is the Strait of Hormuz and Why Does It Matter?” BBC News, 23 June 2025, http://www.bbc.com/news/articles/c78n6p09pzno. Accessed 21 Mar. 2026.

[6] Huangfu, Stella. “Why Surging Oil Prices Are a Shock for the Global Economy – but Not yet a Crisis.” The Conversation , 3 Mar. 2026, theconversation.com/why-surging-oil-prices-are-a-shock-for-the-global-economy-but-not-yet-a-crisis-277228, https://doi.org/10.64628/aa.fwwaf9fms. Accessed 21 Mar. 2026.

[7] Li, Sally. “Iran War Scenarios: The Oil Price That Breaks Parts of the Economy.” Oxford Economics, 13 Mar. 2026, http://www.oxfordeconomics.com/resource/iran-war-scenarios-the-oil-price-that-breaks-parts-of-the-economy/. Accessed 21 Mar. 2026.

[8] Dang, Sheila, et al. “Big Oil to Reap Billions from Iran War Windfall After a Month of Soaring Energy Prices.” Reuters, 26 Mar. 2026, https://www.reuters.com/business/energy/ceraweek-big-oil-reap-billions-iran-war-windfall-after-month-soaring-energy-2026-03-26/. Accessed 31 Mar. 2026.

[9] Ziady, Hanna“Iranian Oil Exports and the Strait of Hormuz.” CNN, 16 Mar. 2026, https://edition.cnn.com/2026/03/16/business/iranian-oil-exports-hormuz-strait-intl-cmd. Accessed 31 Mar. 2026.

[10] “How Iran Is Making a Mint from Donald Trump’s War.” The Economist, 29 Mar. 2026, https://www.economist.com/finance-and-economics/2026/03/29/how-iran-is-making-a-mint-from-donald-trumps-war. Accessed 31 Mar. 2026.

[11] TOI Business Desk. “Iran War Economic Impact: US, China, India, Gulf Countries, Russia, Europe – Who Are the Winners and Losers?” The Times of India, The Times Of India, 12 Mar. 2026, timesofindia.indiatimes.com/business/international-business/iran-war-economic-impact-us-china-india-gulf-countries-russia-europe-who-are-the-winners-and-losers/articleshow/129512724.cms. Accessed 21 Mar. 2026.

[12] Olesya Astakhova, et al. “OPEC+ Agrees Modest Oil Output Boost Even as US War on Iran Disrupts Shipments.” Reuters, 1 Mar. 2026, http://www.reuters.com/business/energy/opec-debates-oil-output-boost-us-war-iran-disrupts-shipments-2026-03-01/. Accessed 21 Mar. 2026.

[13] IEA. “IEA Member Countries to Carry out Largest Ever Oil Stock Release amid Market Disruptions from Middle East Conflict – News – IEA.” IEA, 11 Mar. 2026, http://www.iea.org/news/iea-member-countries-to-carry-out-largest-ever-oil-stock-release-amid-market-disruptions-from-middle-east-conflict. Accessed 21 Mar. 2026.

[14] Hidayat, Muflih. “IEA Emergency Oil Reserves Release: 2026 Crisis Response.” Discovery Alert, 16 Mar. 2026, discoveryalert.com.au/iea-emergency-oil-reserves-release-2026-geopolitical-tensions/. Accessed 21 Mar. 2026.

[15] Ocando Alex, Gustavo. “Drilling Returns to Venezuela’s Lake Maracaibo: Good News for Trump but Locals Still Yearn for Relief.” Monocle, 25 Mar. 2026, https://monocle.com/affairs/oil-drilling-venezuela-lake-maracaibo-trump-iran/. Accessed 31 Mar. 2026.

[16] Burclaff, Natalie. “Research Guides: Oil and Gas Industry: A Research Guide: Organizations and Cartels.” Guides.loc.gov, guides.loc.gov/oil-and-gas-industry/organizations. Accessed 21 Mar. 2026.

[17] Montesquieu, Charles. The Spirit of the Laws. Montesquieu, 1748.

.jpg){kind=link}

Leave a comment