Introduction:

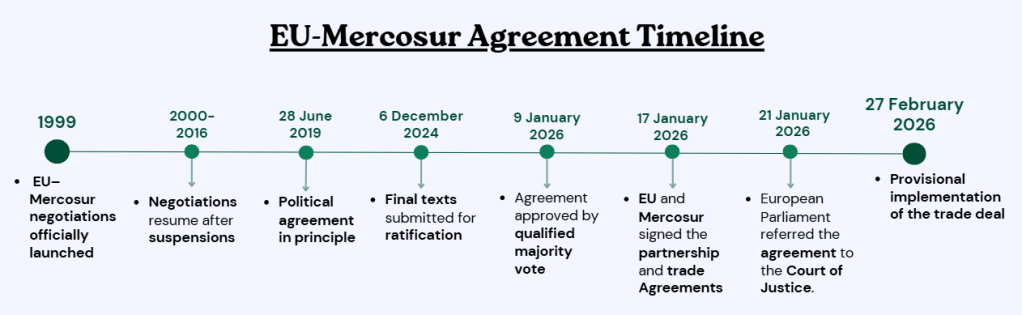

After 25 years of negotiations, the European Union and the Mercosur bloc appeared ready to conclude one of the world’s largest trade agreements in January [1]. That expectation shifted on 21 January 2026, when the European Parliament narrowly voted to refer the deal to the Court of Justice for legal review [2]. Yet only weeks later, the Council moved toward provisional implementation [3]; a decision that reflects the geopolitical context: renewed tariff threats from Washington, the ongoing war in Ukraine and intensifying strategic competition have turned diversification into a strategic objective in its own right. Mercosur promises reduced dependence on China for critical minerals and new outlets for European industry.

The agreement would eliminate most tariffs on industrial and agricultural goods between the EU and Mercosur, a South American bloc comprising Argentina, Brazil, Paraguay, Uruguay and Bolivia linking markets of over 700 million people. Yet, the Mercosur agreement has emerged as one of the most divisive issues in EU politics.

A fundamental question emerges: will this strategic recalibration allow the EU to pursue geopolitical autonomy without weakening the regulatory model that has long defined its political identity?

I) Commerce as a Trojan Horse for Geopolitical Power

| Trading Partner | Total Trade (imports and exports) of GOODS | EU Rank (goods volume) |

| United States | €865 billion | #1 |

| China | €732 billion | #2 |

| Mercosur | €111 billion | #10 |

EU total trade in goods by partner, highlighting the relative weight of Mercosur compared to the United States and China.

In economic terms, Mercosur remains a secondary trading partner for the EU. Goods trade between the two blocs reached approximately €111 billion in 2024, eight times less than trade between the EU and the US. This places Mercosur tenth among EU trading partners, far behind the United States (€865 billion) and China (€732 billion). Even the European Commission’s own projections suggest that the agreement would increase EU GDP by around 0.05 percent by 2040. The macroeconomic stakes are therefore limited.

This asymmetry becomes more striking when viewed from the other side. While Mercosur ranks only tenth for the EU, the EU stands as Mercosur’s second-largest trading partner in goods, behind China. In structural terms, Brussels holds a stronger bargaining position. However, China has steadily expanded its presence in Latin America over the past two decades, surpassing Europe to become the region’s largest trading partner and a major source of infrastructure financing. “Strategically, Mercosur would help the EU diversify beyond China as a source of critical minerals, which are vital for the green transition and defense-related supply chains,” told Max Maton, economist at Oxford Economics, to BBC Mundo.

The agreement thus operates on two levels simultaneously: as a commercial arrangement with long-term projected gains, and as a geopolitical instrument aimed at reducing dependency on China and the United States, reasserting European influence in the world. Whether these strategic objectives justify the regulatory and agricultural compromises required for ratification remains the central tension running through the deal.

II) Who Really Benefits ? Industries Win, Farmers Pay the Price

The agreement’s economic impacts are distributed unevenly across sectors, explaining much of the political opposition it has encountered. The deal is often described as “meat for cars”, as Mercosur would secure expanded access to EU agricultural markets, while European firms would gain entry into a historically protected South American market of over 270 million consumers [5].

For European industry, the gains are concentrated and substantial. Three sectors, automobiles, machine tools, and chemicals, are expected to account for nearly two-thirds of increased European exports to Mercosur by 2040 [8]. The automotive sector represents the clearest winner, with exports projected to triple as current tariffs of 35 percent in Brazil and Argentina will be gradually eliminated over fifteen years, beginning in the seventh year [7]. By contrast, agricultural products are treated far more cautiously.

| Product | Quota volume | % of EU production | Phase-in |

| Sugar (raw cane) | 180,000 tonnes (from Brazil) | ~1.1% | Immediate |

| Beef | 99,000 tonnes(subject to 7.5% tariff) | ~1.5% | Gradual |

| Poultry | 180,000 tonnes | ~1.3% | 5 years |

| Ethanol (fuel/other uses) | 200,000 tonnes | N/A (industrial use) | 5 years |

The table includes the most politically contested quotas. Additional products (rice, honey, ethanol for chemical use) are subject to equivalent phase-in mechanisms.

Crucially, these quotas are staggered and paired with safeguard clauses, allowing tariffs to be reimposed if imports surge or prices fall sharply. In theory, this architecture is designed to smooth adjustment rather than trigger abrupt liberalisation.

Even so, many European farmers argue that the core issue is unfair competition rather than volume alone. South American producers benefit from much cheaper labour and lower sanitary standards than those in Europe, particularly regarding the use of hormones, notes the BBC Mundo [7]. In effect, European farmers face higher regulatory costs without equivalent constraints on competitors.

Thousands of farmers demonstrated in Brussels and Paris for several weeks in December 2025 and after the new year, forcing postponement of the original signing ceremony [8]. In response to mounting opposition, the Commission proposed allowing member states to allocate an additional €45 billion to farmers under the next seven-year budget starting in 2028. This followed an earlier proposal to reduce guaranteed agricultural funding by around 20 percent. The revised package would therefore compensate for roughly half of that decrease compared to the previous budget [12]. The funds would be drawn from reserves initially intended for use after 2030, potentially limiting resources available for other policy priorities.

The distributive pattern is clear: benefits accrue to capital-intensive export industries, while costs fall on geographically concentrated agricultural regions.

III) Too Little, Too Late: The Illusion of Regulatory Protection

France sought to address the asymmetry embedded in the agreement through “mirror clauses”, provisions requiring imported products to meet identical production standards to those imposed within the Union. Their rejection during negotiations was politically revealing. Export-oriented economies such as Germany, Spain and Italy supported the agreement’s commercial logic, while France, Poland, Austria and Ireland, with stronger agricultural constituencies, opposed it.

In response to concerns about regulatory gaps, the Commission has highlighted its audit capacity. “In October 2024, an audit conducted in Brazil by the European Commission raised concerns about the lack of traceability of beef exported by Brazil to the European Union: Brazilian authorities were unable to verify that exports of heifer meat contained no traces of beta-estradiol, a hormone banned in the European Union. Upon receiving the audit, Brazil halted exports of female beef” [9]. The Commission presented this episode as an “example [that] clearly demonstrates the effectiveness of the controls carried out by the European Union at the level of production systems in third countries”. In the agreement presented by the Commission on September 3, it agreed to “a more in-depth dialogue with Brazil […] and committed to increasing the number of audits and inspections in third countries.”

and committed to deepening dialogue with Brazil through a dedicated sanitary standards committee, alongside an increase in third-country audits [9].

Although the case does show that detection mechanisms exist and can trigger corrective action, it also exposes some structural limits. The issue was identified only after exports had taken place, raising questions about how long the traceability gap had persisted and whether non-compliant products may already have entered European supply chains. Rather than demonstrating a fully preventive system, the case underlines a model that remains largely reactive.

The scale of the challenge reinforces this concern. That case involved one hormone, one meat category, from one country. Extending equivalent scrutiny to the full scope of the agreement would amount to spanning multiple product categories across four countries with varying institutional capacities, which represents a far more complex challenge. Mirror clauses would require dense audit infrastructures and continuous transparency; capacities that do not yet exist at the required scale.

But the absence of mirror clauses reflects a deliberate trade-off: mandatory production-standard equivalence would raise costs for European industry reliant on Mercosur inputs, ultimately passed on to consumers, according to the Commission [9]. Hence, the Commission chose industrial competitiveness over agricultural protection, and the safeguard clause is the concession offered in return. The result is a system that prioritises responsiveness over anticipation.

The absence of binding enforcement mechanisms for agricultural protections also extends to the agreement’s environmental commitments. The same architecture repeats itself: provisions are formally present but reliant on consultation rather than automatic sanctions.

IV) The Environmental Blind Spot: Outsourcing Europe’s Ecological Costs.

Environmental concerns have shadowed this agreement since its political conclusion in 2019, when Emmanuel Macron claimed to have secured binding climate commitments from Brazil’´´ then-president Jair Bolsonaro – only to withdraw French support a week later as Amazon wildfires dominated the Biarritz G7 [11].

At the heart of the dispute lies a structural divergence between the two regions’ production models. Mercosur economics remain heavily specialised in agricultural exports – beef, soy and sugar – produced under environmental and sanitary standards that diverge sharply from European requirements. The University of São Paulo estimates that the agreement could increase Brazilian agricultural exports to the EU by between 2 and 7 percent [10]. While modest in percentage terms, such growth could translate into the expansion of soy cultivation and cattle ranching into previously uncultivated areas, particularly in the Amazon.

The underlying trajectory is already visible: between 2010 and 2020, herbicide use in Brazil rose by 128 percent while cultivated land expanded by less than 20 percent [10], reflecting a production model increasingly reliant on chemical inputs rather than productivity gains.

For critics, what makes this harder to defend is Europe’s own role in it. In 2021, the EU exported over 6,840 tonnes of pesticides banned within its own borders to Mercosur countries [10]. The Union also prohibits genetically modified cultivation domestically, yet imports large volumes of transgenic Brazilian soy for animal feed, a crop that accounts for more than half of pesticide use in Brazil. The EU is not merely a passive importer of lower standards; in part, it is their supplier. Brussels argues that the agreement embeds environmental safeguards, including commitments linked to the Paris climate accords and dispute-settlement procedures for sustainability breaches. Yet, these mechanisms rely mainly on consultation rather than automatic sanctions.

Conclusion:

The EU-Mercosur agreement reflects a change of trajectory in how Europe positions itself as a power in an increasingly fragmented global economy. Its geopolitical logic prevails the promised economic benefits: the deal aims to reduce dependency on China and the United States, secure access to critical resources, and reassert influence in a region where it has progressively lost ground. From that perspective, the decision to move forward despite strong internal divisions among members could appear strategically coherent.

Yet, despite having established its identity as a normative power for decades, the EU is willing to accept conditions in its external partnerships that diverge from those it imposes internally. Sustainability commitments remain formally present, but their enforcement relies on dialogue and gradual alignment rather than strict conditionality. This tension is most tangible in the agricultural sector, where European farmers, bound by strict regulatory standards, have to face additional competitive concessions in a series that no budget compensation can fully offset.

This historic deal does not amount to a rejection of Europe’s normative ambitions, but erodes them and will impact the EU’s normative credibility. More than a mere economic alliance, the Mercosur agreement reflects the beginning of a shift in the EU’s global strategy, where political partnerships precede values alignment.

Edited by Dimitri Gellé

References

[1] TV5 Monde. “Traité UE-Mercosur: pourquoi certains pays européens sont opposés à l’accord de libre-échange?”, 17 Dec. 2025

[2] Reuters. “EU lawmakers vote to launch legal challenge to Mercosur trade deal”, 21 Jan. 2026

https://www.reuters.com/video/watch/idRW867921012026RP1/

[3] Euronews. “Von der Leyen to implement contentious Mercosur trade deal despite MEPs’ legal challenge”, 27 Feb. 2026.

[4] Le Monde. “EU-Mercosur deal set to be signed, with or without France’s support”, 7 jan. 2026

[5] Le Monde. “Accord UE-Mercosur : pour l’industrie européenne, des gains réels mais lointains”, 10 Jan 2026

[6] European Commission. EU–Mercosur agreement. Directorate-General for Trade and Economic Security. Accessed 18 March 2026

[7] BBC News Mundo. “Por qué Francia y otros países europeos se oponen al acuerdo entre el Mercosur y la Unión Europea, que creará la zona de libre comercio más grande del mundo”, 16 Jan. 2026

https://www.bbc.com/mundo/articles/cwyrqenr72ro

[8] Le Monde. “Prêt à signer l’accord avec le Mercosur, Bruxelles donne des gages aux agriculteurs”, 6 janv. 2026

[9] European Commission. “Accord commercial UE – Mercosur : distinguer le vrai du faux”, 8 january 2026

[10] Le Monde. “Au Brésil, l’accord UE-Mercosur va se traduire par une « avancée de l’agriculture sur des surfaces non exploitées, notamment en Amazonie »”, 18 january 2026

[11] Le Monde. “Accord UE-Mercosur : cinq questions pour comprendre où on en est”, 27 feb. 2026

[12] Financial Times. “Brussels offers EU farmers €45bn to sweeten Mercosur trade deal”, 7 Jan 2026

https://www.ft.com/content/61fbd405-336c-4fbb-84b2-b79beda668ee

[Timeline] European Commission.

The EU-Mercosur trade agreement

https://commission.europa.eu/topics/trade/eu-mercosur-trade-agreement_en

“EU trade relations with Mercosur. Facts, figures and latest developments.”

Legislative Train Schedule- European Parliament, 20 feb 2026

Also [2] and [9].

[Table 1]

US: (https://ec.europa.eu/eurostat/web/products-eurostat-news/w/ddn-20250311-1 )

Mercosur: https://www.consilium.europa.eu/en/infographics/eu-mercosur-trade/

[Table 2]

EuroFactsheet EU-Mercosur on Agriculture, Sept. 3 2025

[Cover picture]

Personal picture of Jie Wang, taken on February 12, 2026, in Madrid.

Leave a comment